Remy Samuels

A 65-year-old couple will need $395,000 in combined savings to afford the cost of certain Medicare plans in retirement, according to the Milliman Retiree Health Cost Index.

The average healthy 65-year-old retiring in 2024 is projected to spend a significant amount on health care over the course of their remaining lifetime, according to the 2024 Milliman Retiree Health Cost Index.

The two most common health care coverage options chosen by Medicare-eligible retirees are Medicare Advantage and Original Medicare with Medigap plus Part D. A healthy 65-year-old man retiring in 2024 with a MAPD (Medicare Advantage with Rx Drug) plan is projected to spend $128,000 on health care in his remaining lifetime, and a woman with the same coverage is projected to spend $147,000 in her remaining lifetime, according to Milliman.

Health Care Costs on the Rise

To afford these costs, Milliman projected that a man with a MAPD plan needs to have at least $86,000 in savings and a woman with the same coverage needs at least $96,000 in savings. The Milliman Index projected that this is the amount of savings (net of taxes) needed at age 65 to pay a retiree’s remaining lifetime health care “total spend,” assuming an investment return of 3% per year.

For a 65-year-old man retiring in 2024 with Medicare plus Medigap plus Part D, the costs are even higher, as they are projected to spend approximately $281,000 on health care expenses throughout retirement and a woman with the same coverage is projected to spend $320,000.

The difference in cost is largely because women on average live longer than men, according to Milliman. The retired man was projected to live until 88, and the woman until 90, in Milliman’s calculation.

The cost of health care in retirement will also depend on several other factors, Milliman explained, such as when someone retires, where they live during retirement and what Medicare benefit plan they choose. The cost of Medicare Advantage, Medigap and Part D plans can vary greatly by state. For example, in Florida, a 65-year-old retiring in 2024 with a lifespan of 88 can be expected to spend upwards of $340,000 on health care, as opposed to around $260,000 to $280,000 in Texas.

Retirees have less control over factors such as health status or how long they will live – both of which are primary drivers of how much their health care will cost.

Milliman also measured the savings needed for a healthy 65-year-old couple in 2024 compared with 2023. A hypothetical couple retiring in 2024 will need to save approximately $7,000 more than they would have in 2023 if they have Original Medicare plus Medigap and Part D coverage, and $8,000 less if they have a MAPD plan, all else being equal.

How Health Care Costs Have Changed

As a result of the Inflation Reduction Act, there were significant changes to Medicare Part D Rx Drug coverage in 2024. Out-of-pocket expenses were significantly reduced because of the law’s elimination of cost sharing in the catastrophic phase of insurance coverage, but as a result, this increased the plan liability, driving an increase in premiums.

In addition, there has been continued growth in spending on major brand name drugs like GLP-1s – which includes medications like Ozempic and Wegovy – even when only covered for diabetes and not obesity, as well as SGLT2s, that slow heart failure, and certain autoimmune drugs. These costs also contributed to increasing premium and out-of-pocket costs, and the trend is expected to continue over the next couple of years, according to Milliman. Higher prescription drug costs have also increased short-term health care cost expectations over the next couple years.

Impact of Retiring Earlier vs. Later

Most people cannot apply for Medicare until age 65, so retiring early means health care costs can be much higher for the individual. For example, if someone retires five years before they are eligible, at age 60, they can expect to pay 56% more for health care expenses if enrolled in Original Medicare plus Medigap (Plan G) plus Part D, and 86% more for health care expenses if they enroll in a MAPD plan than they would if they waited until age 65 to enroll.

Conversely, delaying retirement allows retirees to boost savings and continue earning income and employer-sponsored benefits like health care. Retiring at age 70, for example, would allow a retiree to pay 29% less on health care expenses than if they retired at 65 and are enrolled in Original Medicare plus Medigap plus Part D. They would pay 30% less for health care with a MAPD plan.

“Healthcare expenses are an important and sometimes overlooked component of retirement planning,” said Robert Schmidt, a Milliman principal and co-author of the Retiree Health Cost Index, in a statement. “By taking a realistic look at their health status and healthcare expenses, and then budgeting accordingly, people can take steps to enjoy a less stressful, financially healthier retirement.”

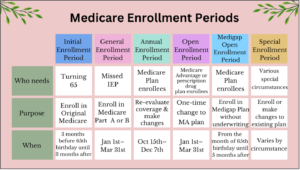

Greg Says is aware that most Medicare beneficiaries find plan option terminology a bit confusing. Please don’t hesitate to reach out to us at InsuranceForOver65 for help in understanding your Medicare plan options especially as we head into the Annual Election Period (Oct. 15 – Dec. 7) during which you can change plans for 2025.

{kind=link}